One of the most valuable things you can have during uncertain markets is perspective.

Yet when headlines intensify, it’s only human to consider moving to cash until things settle down. This feeling is often magnified if you’re approaching retirement or have recently transitioned into it.

The challenge?

Markets don’t send invitations when the best days arrive.

In fact, some of the biggest gains usually happen right when things feel the most uncertain.

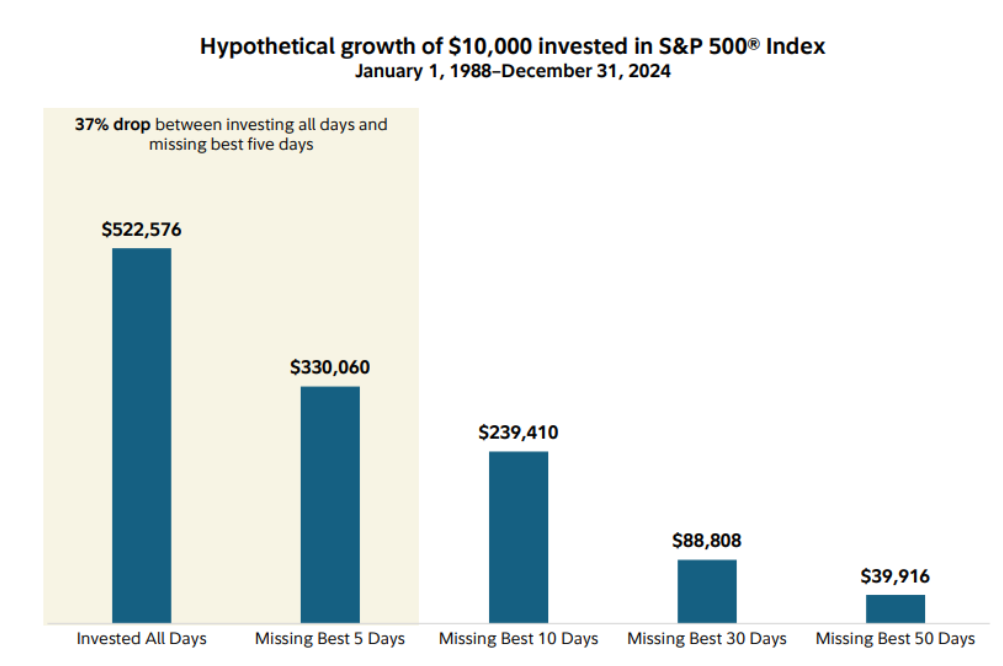

Fidelity shared a chart that illustrates this clearly:

Imagine a $10,000 investment in the S&P 500 back in 1988. That initial amount surpasses $522,000 by 2024, provided you never walked away.

However, missing just the five best market days over that same 37-year period slashes the ending value by roughly 37%.

Find the chart sources and specifications at Fidelity.com1

These few great days are nearly impossible to predict.

What’s more, they often occur shortly after a decline.

Key Goal

Ultimately, our goal is to help you have the resources to live your best retirement life, exactly how you’ve pictured it. Sticking to a disciplined, long-term strategy instead of reacting to headlines is a key component.

For more context behind these numbers, Fidelity breaks it down in this article: 6 reasons why you should consider investing right now.

Reach out with any questions.

–David Bunker, Financial Advisor & Licensed Fiduciary

P.S. In case you missed it, I recently shared my perspectives on the Middle East conflict and what it could mean for your portfolio. Read the post.

Before You Go

Get help optimizing your retirement income. Download our FREE “Prolonging Retirement Income” checklist.

Also, receive help retiring to the life you want, schedule a complimentary financial planning consultation.

This communication was prepared with financial writer Sharron Senter’s assistance, based on interviews with David Bunker, a financial advisor and licensed fiduciary.

Source:

1. Fidelity.com, 6 reasons why you should consider investing right now, https://www.fidelity.com/learning-center/wealth-management-insights/reasons-to-invest-now