In client meetings, we often hear:

“If I have $180,000 a year in retirement, I’m set.”

It’s a great goal.

On paper, it sounds reasonable. But the problem with “magic numbers” is they’re static targets in a moving world.

Fast forward 25 years, and that same $180,000 may only feel like $100,000.

Not because your portfolio failed, but because inflation quietly changed the math.

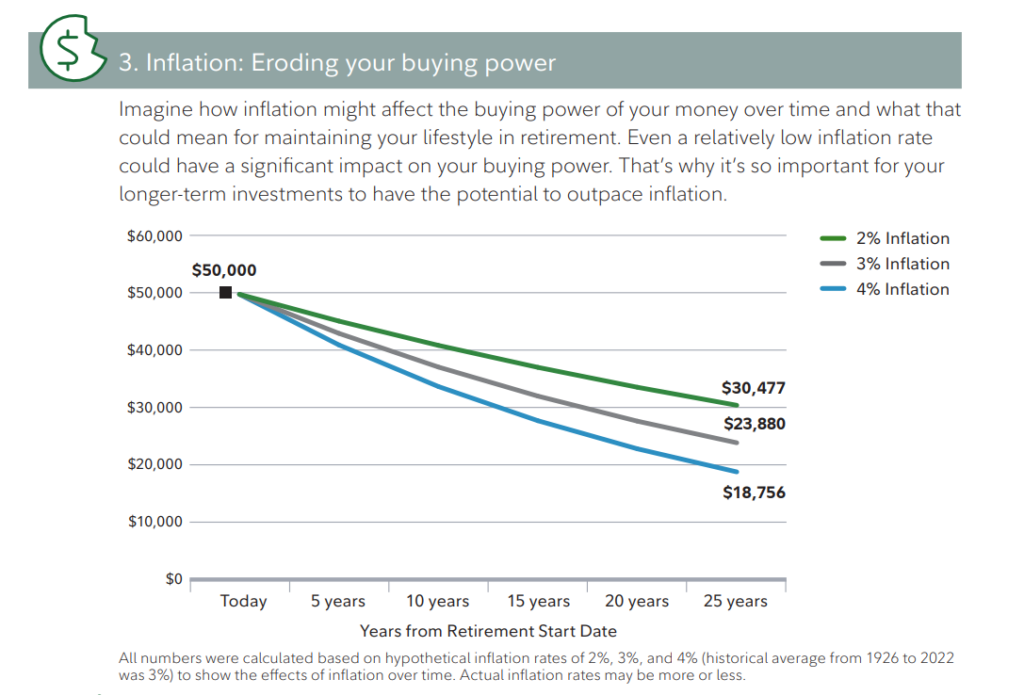

This Fidelity chart highlights the erosion. Even a modest 3% inflation rate can cut purchasing power in half over a typical retirement span:

Inflation compounds over time. And by the time you feel it, your money doesn’t go as far as it used to.

So what do we actually do about it?

For your portfolio, we don’t treat inflation as an afterthought.

We plan for it from the start.

POSITIONING FOR GROWTH

We allocate a portion of your portfolio to assets that have historically outpaced inflation.

In practice, this means focusing on:

- Pricing Power: Investing in companies that can pass rising costs on to consumers, protecting your profit margins.

- Growing Income: Prioritizing dividend-paying companies with track records of increasing payouts to help your cash flow keep pace with rising prices.

- Asset Location: Strategically placing your growth investments in the most tax-efficient accounts, helping to ensure more of your gains remain available for your future spending.

Another Thought

Inflation is just one of the “Big Five” challenges we manage within your retirement strategy.

To see how inflation interacts with the other four (longevity, healthcare, volatility and withdrawals), take a look at this Fidelity breakdown of the Big Five Retirement Risks.

–David Bunker, Financial Advisor & Licensed Fiduciary

P.S. If you’d like to see how inflation and the national debt tie together, read our post: The Guest Who Never Leaves (and wasn’t invited)

Before You Go

Get help optimizing your retirement income. Download our FREE “Prolonging Retirement Income” checklist.

Also, receive help retiring to the life you want, schedule a complimentary financial planning consultation.

This communication was prepared with financial writer Sharron Senter’s assistance, based on interviews with David Bunker, a financial advisor and licensed fiduciary.

Source:

1) Fidelity, Retirement Income Planning, https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/income-diversification.pdf